some positive news out of Canacol En- ergy...just try and not look at the chart. Canacol announced yesterday they are pleased to announce “the results of its Agueda 1 ST exploration well on the Labrador prospect on the LLA23 Exploration and Production ("E&P") Contract, located immediately to the north of the Corporation's Ran- cho Hermoso field in the Llanos Basin of Colombia. Unlike the Rancho Hermoso field, which is governed by contracts with Ecopetrol S.A., the LLA23 contract is governed by the Agencia Nacional de Hidrocarburos, which receives a vari- able base royalty beginning in an 8% related to gross pro- duction resulting in 2-3 times better netbacks and reserve valuations than those available under the Rancho Hermoso tariff and non-tariff contracts. The Corporation has an 80% operated working interest in the LLA23 contract.”

They also add, “A production test of the Lower Gacheta reservoir yielded 1,832 barrels of gross oil per day(1,466 barrels of net oil per day for Canacol) of 28 degree API light oil.”

Meanwhile, the analysts seem to be confused these days—just like everyone else as in the last brief while TD Securities has cut their target on Canacol to $0.85 from $0.95; CIBC has just upped the stock to sector perform with a $0.40 target, up from $0.35; and Mackie Research ups their target to $1.35 from $1.25. One of them might be right.

torsdag 6 december 2012

tisdag 4 december 2012

Intressant forskningsbolag under Vator Capitals paraply

Xbrane Bioscience:s proteinproduktionssystem Lemo, har blivit utnämnt till december månads ”Technical highlight of the month” av SBKB.org, som är ett samarbete mellan Protein Structure Initiative och tidskriften Nature.

Utmärkelsen är ett stort erkännande och beskriver närmare hur Lemos unika egenskaper möjliggör framställningen av olika membranproteiner. Siavash Bashiri, nytillträdd vd för Xbrane Bioscience, ser artikeln som ett användbart skyltfönster mot forskarvärlden.

– Nature är världens mest citerade vetenskapliga tidskrift och räknas till de mest ansedda inom sin nisch. Att bli utsedd till ”technical higlight of the month” är naturligtvis en kvalitetsstämpel och en värdefull referens i vårt framtida arbete, säger Siavash Bashiri.

Starkt förenklat har problembilden tidigare bestått i att forskare endast har kunnat slå på eller av proteinproduktionen i en E. coli-bakterie. Lemo kan liknas vid en dimmer som möjliggör finjustering av produktionshastigheten, vilket innebär att framställningen går att anpassa efter varje enskild proteintyp för att nå maximala produktionsförhållanden.

– Membranproteiner brukar benämnas som ”svåra” proteiner eftersom de är komplicerade eller omöjliga att framställa i vanliga produktionssystem. Det orsakar stora problem för många läkemedelsbolag som är beroende av dessa proteiner i sin forskning. Nu när de ser möjligheterna att producera membranproteiner i vårt system kommer bolagen också vilja testa att framställa sina andra proteiner med vår plattform, säger Siavash Bashiri.

Xbrane Bioscience för i dagsläget dialog med befintliga kunder och flera nya intressenter, främst läkemedelsbolag, som ser potentialen i företagets produkter och nyttan i att få tillgång till kompetensen i team Xbrane.

– Vi ser över en lösning som ska uppfylla bolagens behov ur alla aspekter och effektivisera deras proteinproduktion. Genom att erbjuda en skalbar, kvalitativ och heltäckande servicemodell kring framställning av proteiner, positionerar vi Xbrane Bioscience som en attraktiv aktör på marknaden, med förutsättningar att ansvara för hela proteinproduktionsprocessen, säger Siavash Bashiri.

http://www.sbkb.org/update/2012/12/full/sbkb.2012.113.html

Jeffrey Gundlach, who sees bleak financial times ahead, is the co-founder of DoubleLine Capital.

Fifty billion dollars still sounds like a bunch of money to us. Of course in a day and age when big money managers can attract as much as a trillion dollars, that kind of puts it into perspective.

Bloomberg spent a lot of time this weekend looking at Jeffrey Gundlach and Bloomberg known for its quick/short articles, spent the equivalent of 12 pages on this individ- ual, so obviously there are some people listening to this investor who has made some very interesting calls over the last few years. Like buying mortgage-backed securi- ties right at the bottom of the collapse in housing in the United States.

Gundlach is basically saying that down the road, infla- tion will be back and hard assets will benefit...and for many of us in the beaten up natural gas sector, some of what he is saying sounds a little hopeful to us.

Bloomberg writes, “The co-founder and chief executive officer of DoubleLine Capital LP explains that the first phase of the coming debacle consisted of a 27-year buildup of corporate, personal and sovereign debt. That lasted until 2008, when unfettered lending finally toppled banks and pushed the global economy into a recession, spurring governments and central banks to spend trillions of dollars to stimulate growth...”

“In the ominous third phase” Bloomberg writes, Gund- lach is predicting another crisis: “Deeply indebted coun- tries and companies, which Gundlach doesn’t name, will default sometime after 2013. Central banks may forestall these defaults by pumping even more money into the economy -- at the risk of higher inflation in coming years.”

“Gundlach doesn’t know when the third phase will get here, but he tells his audience they need to gradually get ready for it.”

And again, his whole suggestion is some day, the mar- kets just go—kaboom and you want to be, he suggests, in certain sectors.

He recommends buying hard assets. Gemstones, Art and Commercial Real Estate are high on his list and in his DoubleLine Fund, has also been buying the stocks of Chi- nese companies, U.S. natural gas producers and gold- mining firms because it considers them to be bargains.

If you have time, Google, “Bond Investor Gundlach buys stocks, sees kaboom ahead.”

Bloomberg spent a lot of time this weekend looking at Jeffrey Gundlach and Bloomberg known for its quick/short articles, spent the equivalent of 12 pages on this individ- ual, so obviously there are some people listening to this investor who has made some very interesting calls over the last few years. Like buying mortgage-backed securi- ties right at the bottom of the collapse in housing in the United States.

Gundlach is basically saying that down the road, infla- tion will be back and hard assets will benefit...and for many of us in the beaten up natural gas sector, some of what he is saying sounds a little hopeful to us.

Bloomberg writes, “The co-founder and chief executive officer of DoubleLine Capital LP explains that the first phase of the coming debacle consisted of a 27-year buildup of corporate, personal and sovereign debt. That lasted until 2008, when unfettered lending finally toppled banks and pushed the global economy into a recession, spurring governments and central banks to spend trillions of dollars to stimulate growth...”

“In the ominous third phase” Bloomberg writes, Gund- lach is predicting another crisis: “Deeply indebted coun- tries and companies, which Gundlach doesn’t name, will default sometime after 2013. Central banks may forestall these defaults by pumping even more money into the economy -- at the risk of higher inflation in coming years.”

“Gundlach doesn’t know when the third phase will get here, but he tells his audience they need to gradually get ready for it.”

And again, his whole suggestion is some day, the mar- kets just go—kaboom and you want to be, he suggests, in certain sectors.

He recommends buying hard assets. Gemstones, Art and Commercial Real Estate are high on his list and in his DoubleLine Fund, has also been buying the stocks of Chi- nese companies, U.S. natural gas producers and gold- mining firms because it considers them to be bargains.

If you have time, Google, “Bond Investor Gundlach buys stocks, sees kaboom ahead.”

måndag 3 december 2012

Sino Agro Food ett steg närmare OMX Nasdaq First North

Man har utnämt EPB till financial advisor

http://finance.yahoo.com/news/sino-agro-food-inc-retains-143000198.html

http://finance.yahoo.com/news/sino-agro-food-inc-retains-143000198.html

söndag 2 december 2012

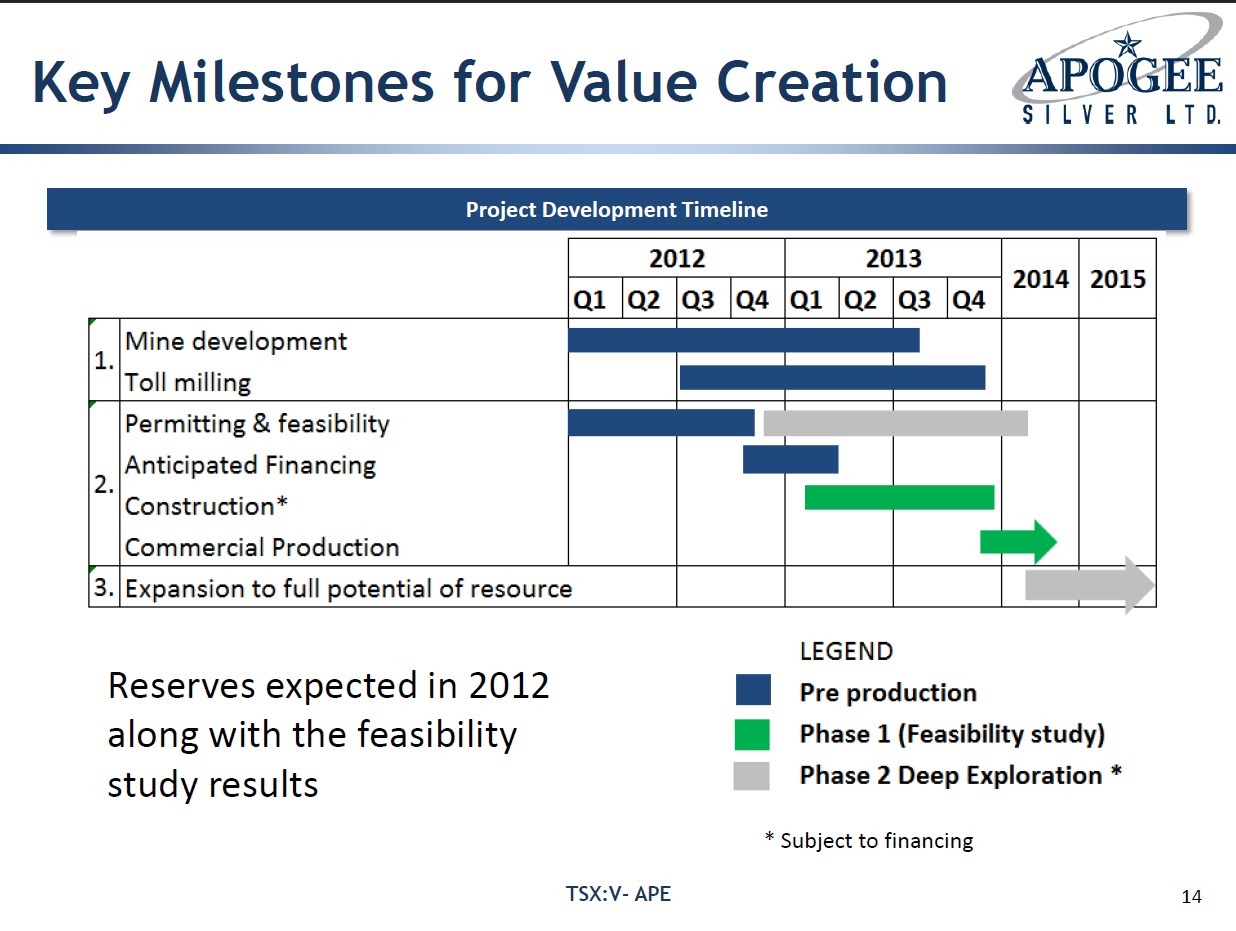

Jämförelse av värdering av Silverbolagen & APE

Taget från Apogee Silvers november presentation

Apogee Silver (APE:TSV)

Jag ligger själv som bekant tung i Aurcana, äger inga Avino för tillfället men efter Aurcana är Avino silver and goldmines det silverbolag som jag är mest positiv till och sugen att ta in i portföljen.

Arian Silver har jag spanat på men valt bort för Aurcana, men Arian förefaller vara ett prisvärt köp med verksamheten i Mexico, har inte full koll på deras ekonomi just nu dock.

För den som vill ta mindre risk men tror på silver framöver är First Majestic förmodligen det klockrena köpet, om inte Aurcana förstås.

Apogee silver är lågt värderat, men det kan förklaras av den höga politiska risken i Bolivia.

Bear Creek har för nåt år sedan fått tillgångar konfiskerade av Bolivias regering.

Det är fullt möjligt att Apogee får behålla sina tillgångar så länge de förblir av "mindre betydelse" ur ett nationellt mining-perspektiv. Säg att politiken förändrats om ett antal år och företaget enl. plan uppnått fullskalig produktion 2014-2015

Apogee Silver (APE:TSV)

Jag ligger själv som bekant tung i Aurcana, äger inga Avino för tillfället men efter Aurcana är Avino silver and goldmines det silverbolag som jag är mest positiv till och sugen att ta in i portföljen.

Arian Silver har jag spanat på men valt bort för Aurcana, men Arian förefaller vara ett prisvärt köp med verksamheten i Mexico, har inte full koll på deras ekonomi just nu dock.

För den som vill ta mindre risk men tror på silver framöver är First Majestic förmodligen det klockrena köpet, om inte Aurcana förstås.

Apogee silver är lågt värderat, men det kan förklaras av den höga politiska risken i Bolivia.

Bear Creek har för nåt år sedan fått tillgångar konfiskerade av Bolivias regering.

Det är fullt möjligt att Apogee får behålla sina tillgångar så länge de förblir av "mindre betydelse" ur ett nationellt mining-perspektiv. Säg att politiken förändrats om ett antal år och företaget enl. plan uppnått fullskalig produktion 2014-2015

France Telecom utdelning historiskt & framöver

På grund av dålig marknad i år och nästa år har man bestämt en minimum utdelning på 0.8 USD, dvs lite drygt 8% för 2013-2014

Utdelningen var mer än dubblan för 2012: nästan 1.8 USD

France Telecom tror på vändning åter till tillväxt 2014. Jag behåller mina France Telecom som nu ligger ca -20%, och kommer köpa mer om kursen faller överdrivet mycket.

Historiken är också bra, åren 1998-2012:

Yahoo Finance - Historisk utdelning

Prices

Utdelningen var mer än dubblan för 2012: nästan 1.8 USD

France Telecom tror på vändning åter till tillväxt 2014. Jag behåller mina France Telecom som nu ligger ca -20%, och kommer köpa mer om kursen faller överdrivet mycket.

Historiken är också bra, åren 1998-2012:

Yahoo Finance - Historisk utdelning

Prices

| Date | Open | High | Low | Close | Volume | Adj Close* | ||||||||||||||||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Sep 4, 2012 | 0.709 Dividend | |||||||||||||||||||||||||||||||||||

| Jun 5, 2012 | 1.049 Dividend | |||||||||||||||||||||||||||||||||||

| Aug 31, 2011 | 0.85 Dividend | |||||||||||||||||||||||||||||||||||

| Jun 7, 2011 | 1.169 Dividend | |||||||||||||||||||||||||||||||||||

| Aug 25, 2010 | 0.794 Dividend | |||||||||||||||||||||||||||||||||||

| Jun 9, 2010 | 1.015 Dividend | |||||||||||||||||||||||||||||||||||

| Aug 25, 2009 | 0.848 Dividend | |||||||||||||||||||||||||||||||||||

| May 28, 2009 | 1.12 Dividend | |||||||||||||||||||||||||||||||||||

| Sep 8, 2008 | 0.883 Dividend | |||||||||||||||||||||||||||||||||||

| May 29, 2008 | 1.891 Dividend | |||||||||||||||||||||||||||||||||||

| Jun 4, 2007 | 1.631 Dividend | |||||||||||||||||||||||||||||||||||

| May 5, 2006 | 1.244 Dividend | |||||||||||||||||||||||||||||||||||

| May 31, 2005 | 0.606 Dividend | |||||||||||||||||||||||||||||||||||

| May 5, 2004 | 0.299 Dividend | |||||||||||||||||||||||||||||||||||

| Apr 15, 2004 | 0.683 Dividend | |||||||||||||||||||||||||||||||||||

| Apr 15, 2003 | 2.756 Dividend | |||||||||||||||||||||||||||||||||||

| Mar 26, 2003 | 0.21 Dividend | |||||||||||||||||||||||||||||||||||

| May 30, 2002 | 0.912 Dividend | |||||||||||||||||||||||||||||||||||

| Jun 12, 2001 | 0.86 Dividend | |||||||||||||||||||||||||||||||||||

| Jun 20, 2000 | 0.953 Dividend | |||||||||||||||||||||||||||||||||||

| Jun 15, 2000 | 0.218 Dividend | |||||||||||||||||||||||||||||||||||

| Jun 15, 1999 | 1.033 Dividend | |||||||||||||||||||||||||||||||||||

| Dec 7, 1998 | 0.23 Dividend | |||||||||||||||||||||||||||||||||||

| Jun 15, 1998 | 1.07 Dividend | |||||||||||||||||||||||||||||||||||

fredag 30 november 2012

DetNor likt lupe klockren på 1-10 års sikt

Det Norske’s Outgoing CEO Sees Value Doubling on Output Surge

By Mikael Holter

november 19, 2012 11:10 fm

Det Norske Oljeselskap ASA (DETNOR) outgoing Chief Executive Officer Erik Haugane said the shares will double by 2015 as reserve estimates are set for the Johan Sverdup oilfield and the company becomes a full-fledged producer.

The 59-year-old, who will next year step down as CEO of the company he founded in 2001, said he will remain a shareholder through his investment company, Koerven AS, which holds 724,414 shares. That represents 0.57 percent of the Trondheim-based company, which is valued at 10.3 billion kroner ($1.8 billion).

“A good deal of the market has short-term investment horizons,” he said in an interview. “I’m at least going to make sure I’m sitting with quite a few shares since I know the upturn is coming.”

The stock has already more than tripled since the company announced the first find on its side of what is now known as the Johan Sverdrup field, which may hold 3.3 billion barrels of oil equivalent. Statoil ASA (STL), which owns 40 percent of both blocks that contain the field, has said new reserve estimates will be released early next year, while a development plan is due in 2014 and an output start in 2018.

Det Norske is transforming itself from an exploration company into an oil producer as pumping is scheduled from fields such as Jette in March next year and Ivar Aasen in 2016. Ivar Aasen, of which Det Norske holds 35 percent, could yield 25,000 barrels of oil a day at its peak in 2018, compared to the company’s output of about 800 barrels of oil equivalent a day in the third quarter, according to its website.

By 2014, when the Sverdrup plan is released and Aasen is two years away from production, it will be “sufficiently short- term for the markets to start to react,” he said.

Swedbank First Securities analyst Teodor Sveen Nilsen, who has a buy recommendation and a target price of 130 kroner, estimated the company’s production will grow to as much as 26,000 barrels a day in 2017 and more than 80,000 barrels a day in 2021.

The shares have dropped from a record close of 98.5 kroner on Sept. 14 to 81.25 kroner as of the 4:30 p.m. close in Oslo.

Det Norske said in October that Haugane would leave after a mutual agreement. Aker ASA (AKER), the biggest owner with 49.99 percent of the shares, said the company needed to improve operationally and strengthen its team in order to become a full oil producer.

Det Norske took a 1.9 billion write-down on the North Sea Jette project in the third quarter after technical problems with a production well. Chairman Svein Aaser said in an interview that organizational changes could in hindsight have been made before the development of the field started.

Haugane said his stepping down had nothing to do with Jette since the departure had been agreed on before the difficulties. He said he would now seek to sit on boards at Norwegian companies and would be unlikely to seek an executive post at a rival company. Det Norske will also likely be his only investment, he said.

“I’m not an investor type,” he said. “It’s not very exciting.”

By Mikael Holter

november 19, 2012 11:10 fm

Det Norske Oljeselskap ASA (DETNOR) outgoing Chief Executive Officer Erik Haugane said the shares will double by 2015 as reserve estimates are set for the Johan Sverdup oilfield and the company becomes a full-fledged producer.

The 59-year-old, who will next year step down as CEO of the company he founded in 2001, said he will remain a shareholder through his investment company, Koerven AS, which holds 724,414 shares. That represents 0.57 percent of the Trondheim-based company, which is valued at 10.3 billion kroner ($1.8 billion).

“A good deal of the market has short-term investment horizons,” he said in an interview. “I’m at least going to make sure I’m sitting with quite a few shares since I know the upturn is coming.”

The stock has already more than tripled since the company announced the first find on its side of what is now known as the Johan Sverdrup field, which may hold 3.3 billion barrels of oil equivalent. Statoil ASA (STL), which owns 40 percent of both blocks that contain the field, has said new reserve estimates will be released early next year, while a development plan is due in 2014 and an output start in 2018.

Det Norske is transforming itself from an exploration company into an oil producer as pumping is scheduled from fields such as Jette in March next year and Ivar Aasen in 2016. Ivar Aasen, of which Det Norske holds 35 percent, could yield 25,000 barrels of oil a day at its peak in 2018, compared to the company’s output of about 800 barrels of oil equivalent a day in the third quarter, according to its website.

By 2014, when the Sverdrup plan is released and Aasen is two years away from production, it will be “sufficiently short- term for the markets to start to react,” he said.

Swedbank First Securities analyst Teodor Sveen Nilsen, who has a buy recommendation and a target price of 130 kroner, estimated the company’s production will grow to as much as 26,000 barrels a day in 2017 and more than 80,000 barrels a day in 2021.

The shares have dropped from a record close of 98.5 kroner on Sept. 14 to 81.25 kroner as of the 4:30 p.m. close in Oslo.

Det Norske said in October that Haugane would leave after a mutual agreement. Aker ASA (AKER), the biggest owner with 49.99 percent of the shares, said the company needed to improve operationally and strengthen its team in order to become a full oil producer.

Det Norske took a 1.9 billion write-down on the North Sea Jette project in the third quarter after technical problems with a production well. Chairman Svein Aaser said in an interview that organizational changes could in hindsight have been made before the development of the field started.

Haugane said his stepping down had nothing to do with Jette since the departure had been agreed on before the difficulties. He said he would now seek to sit on boards at Norwegian companies and would be unlikely to seek an executive post at a rival company. Det Norske will also likely be his only investment, he said.

“I’m not an investor type,” he said. “It’s not very exciting.”

Prenumerera på:

Inlägg (Atom)